As a mother, your top priority is ensuring the safety and well-being of your children. While it may be difficult to think about, it’s important to consider what would happen to your family if something were to happen to you. Life insurance can provide peace of mind knowing that your loved ones will be financially supported in the event of your unexpected passing. As a central figure in your family’s life, your absence could significantly impact their lifestyle, but life insurance can help ease the burden during a difficult time.

How much cover do I need?

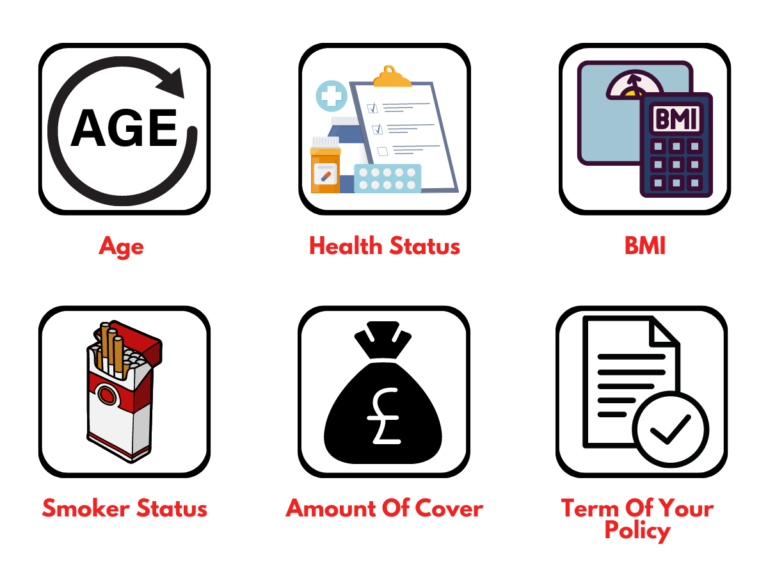

The amount of cover you need is based on your situation. The way how we calculate the amount of cover you need is by taking a look at your expenditure and working out how much your children would need to live the same lifestyle that you provide for them until they are financially independent.

However, sometimes the amount of cover may be significantly high meaning the monthly premiums could be out of budget. That is why we always try to create a balance between what is needed to protect your family and also something affordable for your situation.

What type of life insurance do I need?

Decreasing term insurance:

Decreasing term life insurance is frequently linked to repayament mortgages. The pay out covers the outstanding balance of your mortgage if you pass away.

These policies frequently have lower premiums than level term or whole life policies.

Level term insurance:

Level term policies pay out the same amount regardless of when you die, as long as you pass away during the policy term.

This type of cover is for interest only mortgages and also provides a safety net for your children until they are financially independent. It is important you have this in place especially if you’re a single mum. This ensures that your children can live the same lifestyle that you provided for them until they are financially independent.

Whole of life insurance:

Some mothers want to ensure that their children receive a pay out regardless of when they die, not just during a specific term.

That is why some people decide on a whole of life insurance policy. This policy is usually used to help pay for funeral costs, as the maximum amount of coverage is £10,000.

People choose to write life insurance in trust to decrease the likelihood of having to pay inheritance tax.

This is due to the fact that your insurance is not considered part of your estate. Another advantage is that you avoid the probate stage. This essentially means that your family will receive their money sooner.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

No Comments