Self employed income protection (1) insurance works by giving you a percentage of your regular income if you’re unable to work i.e. getting sick or hurt. However, it doesn’t cover you for redundancy nor disciplinary actions.

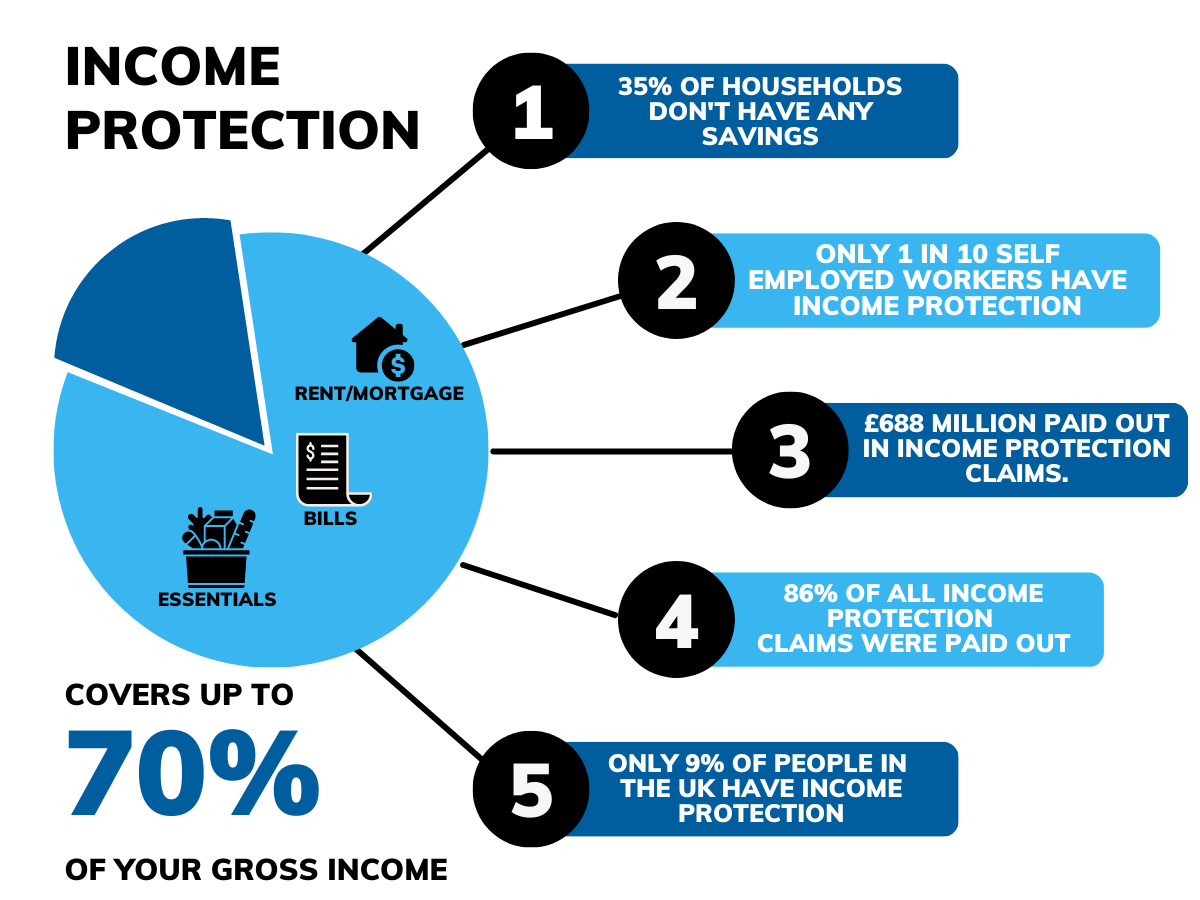

Generally, you will get between 50 and 70% of your typical income, but this can change from provider to provider.

You won’t get a lump sum payment (2). Instead, you’ll get payments every month that aren’t taxed. Overall, this can help you make ends meet while you can’t work.

Evidently income protection is very important, as when you are self employed you receive no sick pay.

Your payments will continue to come until one of the following happens first:

Ask yourself, would you be able to get by with £99.35 (3) a week while you are unable to to work and receive your monthly income?

Why do I need self employed income protection?

Firstly, if you can’t work, your finances can suffer a lot. Thus making it hard to make ends meet without your usual income.

Evidently, income protection insurance is a good idea for anyone who is worried about what would happen if they got sick or hurt and couldn’t work. Hence, why we recommend it.

Overall income protection insurance can help by replacing lost income as a result of being unable to work. Thus allowing you to maintain your present lifestyle with minimal financial hardship.

Who does self employed income protection insurance benefit?

Self Employed

Somone with little to no savings

A person with no other source of income

Someone with no sick pay

Who does income protection insurance benefit?

Self Employed

Somone with little to no savings

A person with no other source of income

Someone with no sick pay

What determines the cost of self employed income protection?

Age

Policy type

occupation

Smoker Status

Medical History

Length of deferred period

Due to the fact that your premium is determined using information that is specific to you, the cost of income protection insurance will therefore vary from person to person.

What can income protection insurance help you cover?

Rent or Mortgage

Household Bills

Living Costs

Grocery shopping

Any Debt payments

Leisure

Other essential costs.

Self employed income protection

Generally speaking, Income protection is especially crucial. Particularly, for the self-employed, as they lack the financial certainty that typical sick leave benefits provide.

Therefore, many people who are self-employed run the risk of losing out on income that cannot be replaced if they become ill or injured, or they run the risk of having to return to work before they have fully recovered in order to maintain their current standard of living.

What doesn’t self employed income protection cover?

Illnesses caused by drugs or alcohol

Pre-existing conditions

Self inflicted injuries

Unemployment

Redundancy

How long does income protection pay out for?

'Payment period'

The payment period is the maximum amount of time your income protection policy will pay your monthly allowences for if you’re unable to work due to sickness or an accident.

However, to file a claim for the same condition again, you must normally return to work for a period of time, which is usually 6 months.

Generally there are several possibilities for Income Protection coverage. Payment durations are often 12 months, 24 months, 60 months, or until the insurance expires.

For the last option, the expiration of the policy is normally associated with your retirement age.

If you have a policy with a payout period to the end of the policy life, a claim could last until retirement if you are undoubtedly unable to ever return to work again.

When thinking about the duration of the payout period. It is important to note that it is usually determined by your budget. Subsequently the longer the payment period, the greater the monthly premium charged by the insurer. Each recommendation on the payment period differs between each individual. In reality finding the right duration is dependent on finding a balance between how comprehensive your cover is and your budget.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

No Comments